How Much Should Your Emergency Fund Actually Be?

Most people get this wrong. We break down the math for different life situations — from freelancers to families to single-income households.

Read ArticleSpeed matters when emergencies hit. This guide explains how to structure your funds so you can actually access money quickly without penalties or delays.

Liquidity isn’t just a financial term you hear bankers throw around. It’s literally how quickly you can get your hands on your money when you need it most. When an emergency hits — and they always do — the last thing you want is to discover your cash is locked up in a fixed deposit for another 8 months.

Think about it this way: money sitting in your savings account is highly liquid. You can withdraw it the same day, sometimes within minutes. But money in a 5-year fixed deposit? That’s illiquid. You’ll face penalties and waiting periods if you break it early. Your emergency fund needs to live somewhere in between — accessible enough for real emergencies, yet earning decent returns.

We’re going to walk through exactly how to set this up so your emergency money is there when you need it, without unnecessary friction.

Different types of accounts give you different speeds. You’ll want a mix of all three.

Your regular bank savings account. Withdraw same-day or within hours. Interest rate? Usually terrible — maybe 3-4% per year. But that’s fine because you’re only keeping a small slice of your emergency fund here. Think 10-20% of your total.

Mutual fund investments that you can withdraw in 1-2 business days. Returns are typically 5-6% annually, which beats savings accounts by miles. This is where the bulk of your emergency fund should live — maybe 60-70% of it. You’re getting reasonable returns without sacrificing accessibility.

Fixed deposits with 6-month to 1-year maturity. You can break them early if absolutely necessary, though you’ll lose some interest. Returns hit 6-7% easily. Keep 15-25% of your emergency fund here — money you’re less likely to touch but want ready if needed.

Here’s the setup that actually works. You’re not putting all your eggs in one basket, and you’re not making access so complicated that you avoid tapping into your fund when you genuinely need it.

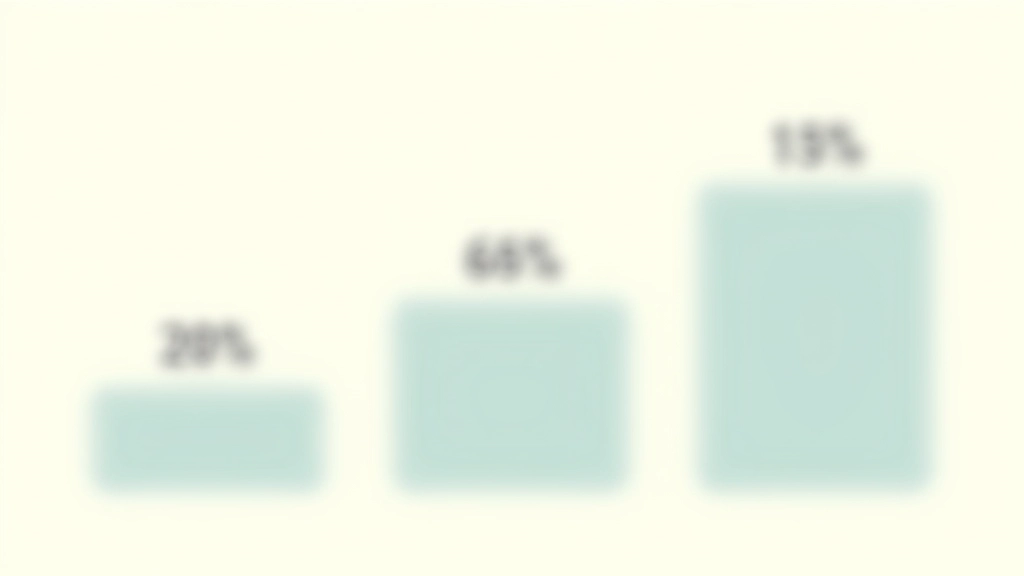

Keep 20,000-30,000 depending on your monthly expenses. This is your first line of defense. Medical emergency at 2 AM? You don’t want to wait until the bank opens.

The bulk lives here. Better returns than savings, still accessible in 1-2 days. Most emergencies you’ll ever face can be handled from this bucket. Job loss, car repair, medical bills — liquid funds cover it.

These mature gradually. When one FD matures, reinvest it or let it sit in your savings account temporarily. It’s your buffer that’s working harder but still accessible if you really need it.

Stop overthinking it. You don’t need fancy apps or complex strategies. Here’s what to do this week.

First, make sure your primary savings account offers reasonable rates. If you’re earning 2% per year, you’re getting robbed. Switch to HDFC, ICICI, or even SBI if they offer better rates. You want at least 4% on your savings account balance. Takes 15 minutes to open an account online.

You’ll need a brokerage account. Zerodha, Groww, or even your bank’s app works. Invest in a liquid fund — look for funds with names like “ICICI Liquid Fund” or “HDFC Liquid Fund”. These funds invest in short-term securities and let you withdraw in 1-2 business days. Start with whatever you can invest right now. 10,000? 50,000? It all counts.

Once your liquid fund has grown, open 2-3 short-term fixed deposits. Not 5-year ones — 6-month or 1-year terms. Different banks, different maturity dates. So one matures in June, another in September, another in December. This way you’re not trying to break one early if you need the cash.

When each FD is about to mature, you’ll get a notice. Don’t let it auto-renew into a long-term deposit. Either reinvest it in a new 6-month FD, or let it sit in your savings account temporarily. You’re actively managing this now, not letting it go on autopilot.

We’ve seen these slip-ups over and over. You don’t have to make them.

Yes, the interest rate looks beautiful. 7.5% annually sounds amazing compared to 5% in liquid funds. But here’s what happens: you get a hospital bill for 75,000 and you’re breaking that FD early, losing interest and potentially getting charged a penalty. Now your emergency fund actually cost you money to access. Don’t do this.

Safety? Sure, it’s safe. But you’re earning 3-4% when you could be earning 5-6%. Over 5 years on 3,00,000, that’s a difference of 30,000-40,000. That’s real money you’re leaving on the table. Liquid funds aren’t risky — they’re backed by actual securities and SEBI regulations.

When you earn interest from liquid funds or FDs, you’ll owe tax on that interest. It’s not huge, but it matters. Keep records of your interest earned. Liquid funds might have slightly better tax treatment than FD interest depending on your income bracket. Don’t ignore this — your accountant will thank you.

Liquid funds invest in money market instruments and commercial paper. They’re not stocks. Your principal isn’t going to swing by 20% in a month. They’re boring, safe investments that just happen to beat savings accounts. The hesitation people have about them is pure psychology.

“The goal isn’t to hide your emergency money where you can’t find it. The goal is to have it accessible when you actually need it, earning decent returns while you wait. That’s what good liquidity structure does.”

The best emergency fund structure is the one you’ll actually use. If your money is so locked up that you avoid touching it during real emergencies, you’ve defeated the purpose. If your money is earning nothing while sitting idle, you’re wasting opportunity.

The 20-65-15 split we’ve talked about works because it balances both concerns. Your money is there when you need it. Your money is working for you while you wait.

Start small if you need to. 10,000 in a savings account, 20,000 in a liquid fund, a small FD if you can swing it. Build from there. Within 6-12 months of consistent saving, you’ll have a real emergency fund with real liquidity. And when something unexpected happens — and it will — you’ll be ready.

That peace of mind? That’s worth more than the extra 1% interest you might squeeze out elsewhere.

This article is informational only and not financial advice. Interest rates, investment returns, and tax treatment change frequently and vary based on individual circumstances. The allocation percentages (20-65-15) are general guidelines — your specific situation may require adjustments based on your income, expenses, family size, and job stability.

Before making any investment decisions, consult with a qualified financial advisor who understands your complete financial picture. All investments carry risk. Past performance doesn’t guarantee future results. The information here was accurate as of March 2026 but may change.